Posted inBanking

Choose a bank Canada newcomer How to Choose a Bank in Canada as a Newcomer: Your 2026 Guide

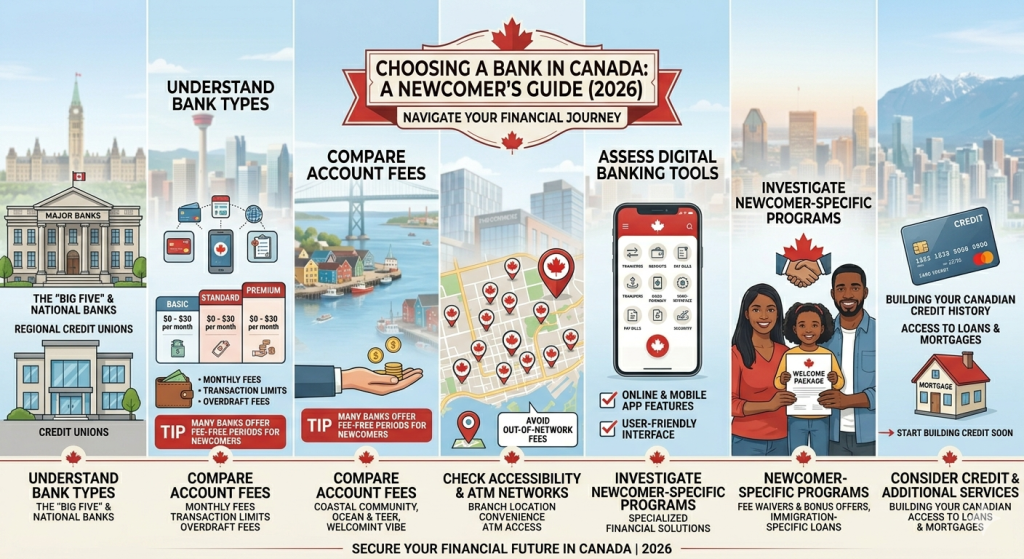

Choosing the right bank in Canada as a newcomer is a crucial step. This guide helps you compare options, understand fees, and find the best financial fit for your first year.