Choose a bank Canada newcomer is a practical topic for newcomers who want clear , begi

er-friendly information about their first year in Canada.

Introduction: Your Financial Fresh Start in Canada

Welcome to Canada! As you embark on this exciting new chapter, one of your very first and most important tasks will be setting up your finances. Learning how to choose a bank Canada newcomer can feel like a big decision, especially with so many options available. But don’t worry , you’re not alone! This comprehensive guide from FirstYearCanada.com is designed to demystify the process and help you make an informed choice that suits your needs .

Getting your banking sorted early is essential for everything from receiving your first paycheck to paying your rent and managing your daily expenses. We understand that navigating a new financial system can be overwhelming, so we’re here to provide clear, practical, and supportive advice .

Who This Guide Is For

This guide is specifically crafted for:

- New permanent residents (PR): Individuals and families making Canada their new home.

- International students: Those pursuing education and needing to manage tuition and living expenses.

- Temporary foreign workers: Individuals on work permits who need a reliable way to receive wages and handle transactions.

- Anyone establishing their first financial presence in Canada: If you’re new to the Canadian banking system, this guide is for you .

Our goal is to help you feel confident and empowered as you take this vital step towards financial stability in Canada. For a broader view of your initial steps, check out our First Month in Canada: Your Essential Checklist for Newcomers.

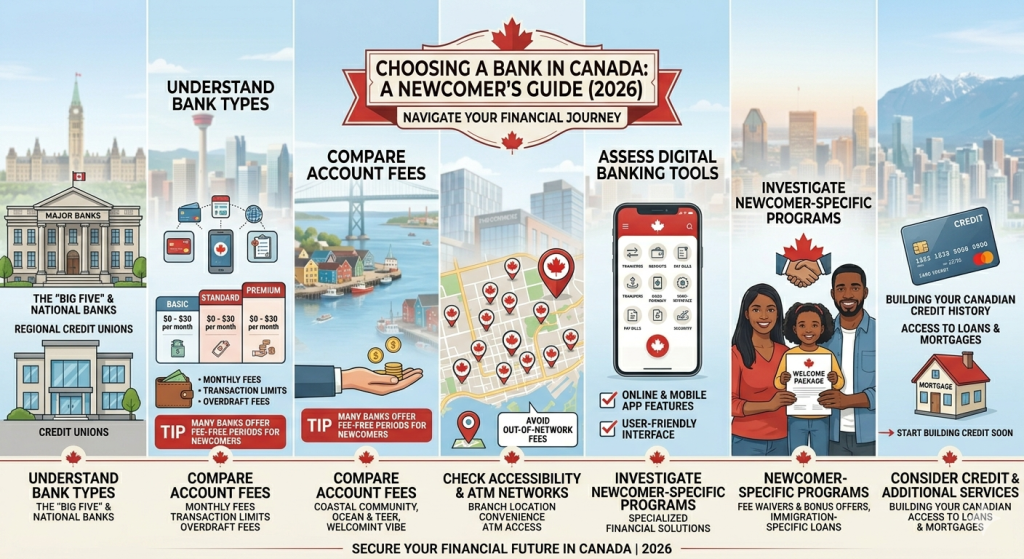

Understanding the Canadian Banking Landscape

Canada’s banking system is robust and reliable. You’ll primarily encounter a few types of financial institutions, each with its own characteristics :

- Major Banks (The ‘Big Five’ and others): These are large, national banks like Royal Bank of Canada (RBC), Toronto-Dominion Bank (TD), Bank of Nova Scotia (Scotiabank), Bank of Montreal (BMO), and Canadian Imperial Bank of Commerce (CIBC). National Bank of Canada is also a significant player, particularly in Quebec. They offer extensive branch networks, a wide range of products (chequing, savings, credit cards, loans, mortgages, investments), and robust digital banking platforms.

- Credit Unions: These are member-owned financial cooperatives that operate locally or regionally. They often prioritize community involvement and may offer more personalized service. While their branch networks might be smaller than the major banks, many offer competitive rates and lower fees.

- Online-Only Banks/Digital Banks: These institutions operate entirely online, without physical branches. They typically offer lower fees, higher interest rates on savings, and excellent digital tools. Examples include EQ Bank and Simplii Financial (a division of CIBC) or Tangerine (a subsidiary of Scotiabank). The trade-off is the lack of in-person service.

Key Factors When You Choose a Bank Canada Newcomer

To make the best decision for your unique situation, consider the following:

1. Fees and Charges

This is often the first thing newcomers look at, and for good reason. Canadian banks charge various fees, including:

- Monthly Account Fees: Many chequing accounts have a monthly fee, which can range from $4 to $30, depending on the number of transactions and services included.

- Transaction Fees: Some accounts have limits on free debit transactions or Interac e-Transfers. Going over these limits incurs extra charges.

- ATM Fees: Using an ATM that isn’t part of your bank’s network can result in fees from both your bank and the ATM operator.

- Other Fees: Look out for fees for overdraft protection, paper statements, foreign currency conversion, or wire transfers.

Tip: Many banks offer fee waivers if you maintain a minimum balance or have certain products with them. Crucially, many also have special newcomer banking packages that waive monthly fees for the first 1-2 years and offer unlimited transactions.

2. Services and Products Offered

Beyond basic chequing and savings accounts, consider what other financial services you might need:

- Chequing Account: For daily transactions, bill payments, and receiving deposits (like your salary).

- Savings Account: For storing money and earning interest.

- Credit Cards: Essential for building your Canadian credit history. Look for secured credit cards or newcomer-specific credit cards if you don’t have a credit history. (Learn more in our guide: Building Credit in Canada: A Newcomer’s Guide) .

- International Money Transfers: If you plan to send money home, compare fees and exchange rates.

- Other Needs : Do you anticipate needing a loan, mortgage, or investment advice in the future?

3. Accessibility and Convenience

- Branch Network: If you prefer in-person service, need to deposit cash frequently, or feel more comfortable speaking with a teller, a bank with branches near your home or workplace might be ideal.

- ATM Access: Ensure easy access to your bank’s ATMs to avoid extra fees.

- Digital Banking: A strong mobile app and online banking platform are almost essential today. Check for features like mobile cheque deposit, bill payment, and Interac e-Transfer.

- Customer Service: Consider the availability of customer support (phone, chat, email) and language options.

4. Newcomer Programs and Offers

This is a significant factor for new arrivals. Most major Canadian banks offer specialized packages for newcomers, which often include :

- Waived monthly account fees for a period (e.g., 12 months, 24 months).

- Unlimited debit transactions and Interac e-Transfers.

- Access to a credit card without a Canadian credit history (often a secured credit card or a low-limit card with specific conditions).

- Free safety deposit box for the first year .

- Multilingual support.

These offers can save you a substantial amount of money in your first year or two.

Step-by-Step Guide to Choosing Your Bank

- Assess Your Needs: Before you even look at specific banks, think about your financial habits. How often will you use your debit card? Do you need to send money internationally? Will you primarily bank online or in-person? What is your budget for monthly fees ?

- Research Newcomer Packages: Visit the websites of the major banks (RBC, TD, Scotiabank, BMO, CIBC, National Bank) and credit unions. Look specifically for their “newcomer,” “immigrant,” or “international student” banking packages.

- Compare Fees and Features: Create a simple comparison chart (or use ours below!) to weigh the pros and cons of each bank’s newcomer offer. Pay close attention to monthly fees after the promotional period, transaction limits, and credit card options.

- Consider Branch Location and Digital Tools: If in-person support is important, find out if there’s a branch conveniently located for you. If you prefer digital, test out their app’s user-friendliness (some banks allow you to explore their app without an account).

- Gather Required Documents: To open an account, you will typically need two pieces of identification, including one government-issued photo ID, and your immigration document (e.g., Permanent Resident card, study permit, work permit). You might also need proof of address. Our guide, How to Open a Bank Account in Canada as a Newcomer 2026 Guide, provides a detailed list.

- Visit a Branch or Apply Online: Once you’ve narrowed down your choices, consider visiting a branch to speak with a banking advisor directly. This is a great opportunity to ask questions, clarify terms, and get a feel for their customer service. Some banks allow you to start the application process online before your arrival or complete it entirely digitally if you meet certain criteria .

- Ask Targeted Questions: Don’t be shy! Ask about:

- The exact fees after the newcomer offer expires.

- How to upgrade your account later if your needs change.

- Options for building credit.

- International money transfer services and fees.

- Online and mobile banking features.

Comparative Overview of Canadian Financial Institutions for Newcomers

Here’s a general overview to help you choose a bank Canada newcomer, focusing on typical characteristics:

| Feature | Major Banks (e.g., RBC, TD, Scotiabank) | Credit Unions (e.g., Vancity, Meridian, Desjardins) | Online-Only Banks (e.g., EQ Bank, Simplii, Tangerine) |

|---|---|---|---|

| Branch Network | Extensive, nationwide | Regional or provincial, often smaller | None (fully digital) |

| Newcomer Programs | Common, often generous fee waivers and credit card access | Some offer, but varies widely by institution | Less common, focus on low fees for all customers |

| Fees | Higher standard monthly fees, often waived for newcomers initially | Generally lower standard fees, community-focused | Typically no monthly fees, high interest on savings |

| Services | Full suite: chequing, savings, credit, investments, mortgages | Comprehensive, but may have fewer specialized investment products | Primarily chequing, savings, investments (often GICs), some credit products |

| Customer Service | Standardized, multilingual support, various cha

els |

Often personalized, community-focused, local support | Primarily digital (chat, email, phone), self-serve |

| I

ovation/Digital |

Strong, constantly evolving apps and online platforms | Varies, some are very modern, others less so | Core strength, user-friendly apps and online experience |

| Credit Building | Clear pathways, specific newcomer credit cards | May offer secured credit cards, varies by institution | Limited direct credit products, often partner with traditional lenders |

Common Mistakes to Avoid When Choosing a Bank

- Not Comparing Options: Settling for the first bank you encounter without exploring other newcomer offers can mean missing out on significant savings and benefits.

- Ignoring Fees After the Promotional Period: While newcomer offers are great, ensure you understand the fees that will apply once the promotional period ends. Plan for this in your Cost of Living in Canada budget.

- Underestimating the Importance of Credit: Building a Canadian credit history is vital for many aspects of life, from renting an apartment to getting a phone plan. Choose a bank that offers clear pathways to credit, even if it’s a secured card initially.

- Not Asking Enough Questions: Don’t be afraid to ask banking representatives about anything you don’t understand. It’s their job to help you.

- Delaying Your Bank Account Setup: You’ll need a bank account for almost everything – receiving your salary, paying bills, and managing daily expenses. Set it up as soon as possible after arrival.

Frequently Asked Questions (FAQ)

Q: Can I open a bank account before arriving in Canada?

A: Most Canadian banks require you to be physically present in Canada with your original immigration documents to open a full bank account. However, some major banks offer “pre-arrival” services where you can start the application process online and have an account partially set up, allowing you to transfer funds to Canada. You’ll still need to visit a branch upon arrival to finalize the account opening and verify your identity.

Q: What documents do I need to open a bank account in Canada?

A: You typically need two pieces of identification. One must be a government-issued photo ID (like your passport). The second piece can be your Permanent Resident card, study permit, or work permit. You might also need proof of your Canadian address (e.g., a lease agreement, utility bill, or official letter). For a detailed list, please refer to our guide on How to Open a Bank Account in Canada as a Newcomer 2026 Guide.

Q: Are my deposits safe in Canadian banks?

A: Yes, very safe. Deposits made at member institutions (which include all major banks and most credit unions) are insured by the Canada Deposit Insurance Corporation (CDIC) or a provincial equivalent (for credit unions). CDIC insures eligible deposits up to $100,000 per depositor per institution, for different categories of deposits. Always check if your chosen institution is a CDIC member.

Q: Should I get a credit card right away?

A: Absolutely! Getting a credit card, even a secured one, as soon as possible is highly recommended. It’s the most effective way to start building your Canadian credit history, which is crucial for renting an apartment, getting a phone contract, buying a car, or even securing future loans. Many banks offer specific credit card options for newcomers. Our article Building Credit in Canada: A Newcomer’s Guide has more details.

Q: What is the difference between a chequing and a savings account?

A: A chequing account is designed for day-to-day transactions like paying bills, making purchases with your debit card, and receiving direct deposits (like your salary). It usually offers easy access to your money but may have lower or no interest earnings. A savings account is meant for storing money you don’t need immediately. It typically earns interest on your balance but might have limits on free transactions or require a higher minimum balance.

Important Disclaimer

This article is for general information only and does not provide financial, legal, tax, or immigration advice. Rules, requirements, fees, and programs may change. Always check official sources or speak with a qualified professional before making decisions.

Sources and Official Resources

- Financial Consumer Agency of Canada (FCAC): Offers unbiased information about financial products and services. www.canada.ca/en/financial-consumer-agency. html

- Canada Deposit Insurance Corporation (CDIC): Provides information on deposit protection. www.cdic.ca

- Major Canadian Bank Websites: For specific newcomer packages and current offers (e.g., RBC, TD, Scotiabank, BMO, CIBC, National Bank of Canada).

- Provincial Credit Union Websites: For details on local credit unions and their services (e.g., Vancity, Meridian Credit Union, Desjardins).

Conclusion

Choosing the right bank is a foundational step in building your new life in Canada. By taking the time to research, compare options, and understand the benefits of newcomer programs, you can make a decision that supports your financial well-being from day one. Remember, you don’t have to navigate this journey alone.FirstYearCanada.com is here to provide you with reliable, practical information every step of the way. We wish you all the best in your financial journey as a newcomer to Canada